Action Plan: What To Do with My Optometry Student Loans Before 2023?

Our inbox has been getting slammed with ODs asking for advice on what to do with their federal student loans as we get closer to the 0% forbearance expiration date of 12/31/22. Politics aside, based on the most recent federal news which removes a lot of uncertainty that we had last month, we are going to break it down with some actionable plans that optometrist can take:

Overview of Current Student Loan Climate:

-

Final extension of student loan repayment & 0% interest pause forbearance until 12/31/22. The Department of Education is informing borrowers that they will start preparing back their federal loans (~6.8% average) after 12/31/22.

-

On Weds 11/2/22, the feds announced 0.75% Rate spike for the sixth time this year, with 0.50% spike in December 2022, and another final one of 0.25% in Feb 2023. After this, the Feds will wait and see how the economy/inflation will react. This will drastically increase student loan refinancing rates after 12/1/2022, and even higher in February 2023.

-

Currently refi student loans are 2.50% Var | 3.11% Fixed. Special Promo (expires 12/31/22) Sofi has 0.875% Discount promo, and Laurel Road’s rates can be even lower but requires a checking account deposit. Consider Refi before 11/30/22

-

IDR accounts adjustment will extend many of the limited PSLF waivers to July 2023

-

Federal loan forgiveness up to $10,000 for practicing ODs (less than $125,000 AGI or <$ 250,000 married). Application is open, but debt discharge is paused due to court order until further notice

-

Five Student Loan Action Plans for Optometrists

What are the lowest student loan refi rates and best deals?

With the recent federal rate increase of 0.75% announced last Wednesday and 2 more planned on 12/14/2022 (+0.50%) and the last one (+0.25%) on 1/31/2023, we are expecting a significant increase in refi rates. So if you are not pursuing federal student loan forgiveness due to a good debt-to-income ratio (less than 3 to 1), then now it is the best time to refinance.

Please be aware that refi rates will never be as low as the 2-3% back in 2020, but will be significantly lower than the 6.8% federal rates after the forbearance expires on 12/31/22. After meeting with all our lender partners, all refinancing rates WILL INCREASE after 12/1/2022, but great news! Refi rates are locked at the beginning of each month, so consider refinancing prior to 11/30/22.

| When to Refinance Student Loans? | Federal Rate Hike Announcement | Change from Today’s Rate | Average Lowest Rates Offered (5 years) |

|---|---|---|---|

| Before 11/30/22 | 0.75% Hike in Nov 3 | 0% Baseline | 2.50% Variable | 3.36% Fixed |

| Before 12/31/22 | 0.50% Hike in Dec 14 | +0.75% higher | 3.25% Variable | 4.11% Fixed |

| Before 01/31/23 | 0.25% Hike in Jan 31 | +1.00% higher | 3.50% Variable | 4.36% Fixed |

| Before 02/30/23 | 0% Hike (unless needed) | +1.00% higher but stable | |

| *Remember that student refi rates are locked in for a whole month at the beginning of each month | |||

All lenders are expecting a significant flood of applications in early 2023 and will be more selective in their approval process. So we expect less rate discounts, lower cash bonuses and even stricter denial of applicants.

Remember that even the financially-savvy Dat Bui was denied by multiple student refi lenders back in 2016 due to stricter lending requirements. The last few years, applications have been quite lax with higher approval rates for doctors, but remember that during times of recession, loan borrowing will get harder.

| Here are the 3 best student refi deals that we negotiated for ODoF members: | |||

|---|---|---|---|

| Student Loan Refi Lenders | ODoF Member Discount | Lowest Rate with all discounts applied (5 years) | CLICK FOR RATE CHECK |

|

$1,000 Bonus or AOA 0.25% discount | 3.97% Var | 1.98% Fixed* | Click Here |

|

0.875% discount† | 3.11% Var | 3.11% Fixed | Click Here |

|

$1,000 Bonus | 2.50% Var | 3.99% Fixed | Click Here |

| *Laurel Road | Require $7.5K Checking account deposit (up to 0.55% total discount) | |||

| †0.375% Discount Promo Expire 12/31/22 + additional 0.50% discount for loans >$150K | |||

Financial Pearl

"We recommend doing a quick online rate quote check (5-10 minute, soft credit pull) with all three lenders to compare and get an overview of your personal market rate, based on your debt-to-income ratio, credit score (Ideally 740+ to get a decent rate), student loan history, etc. For additional help, check out "OD's Guide To Student Refi"

Why should I refinance my students when the government will just forgive all my federal student loans?

It was definitely an unexpected surprise to everyone when Biden announced the $10,000 forgiveness. But was it a surprise when the loan discharge got blocked in federal court? NOPE.

Politics aside, we are still a very divided country, so any legislation or executive order like student loan forgiveness will face opposition, and take a long time to get approved. Remember that the next administration in 11/2024 might not have student loans as their priority.

From an economical aspect, we are heading toward a deeper recession in 2023 with an all time high inflation rate of 8.2%, which is nowhere close to the 2.5% goal of the feds. That being said, we don’t see the treasury being too motivated to give out any more free money.

So overall, don’t let “potential” political promises change your financial plan when it comes to managing your student loans.

Financial Pearl

"One-time debt relief like the $10,000 student forgiveness is completely different from permanent federal forgiveness programs such as 10 year PSLF (usually reserved for ODs working in non-profits like VA or IHS settings) or 20-25 Total Federal Loan forgiveness (if your DTI is greater than 3:1). We actually think these troubled programs will get better with time to avoid any uncertainty.

For more information, read here about the type of federal forgiveness programs"

ACTION PLAN: What should I do with my current student loans?

Throughout these last few years, the most successful & wealthiest optometrists that we know are those who live on significantly less than they make, have a goal to pay off their massive student loans in 5-10 years, have a solid financial game plan, and build wealth along the way.

Hence, why we have taught and advocated for optometrists, especially new ODs graduates, to take charge of their own financial destiny and NOT rely on the uncertainty of government programs. Some of these new student loan policies being proposed will cause more harm than good because it creates so much uncertainty and confusion for borrowers on next steps to take.

Scenario #1: Optometrists with Federal Student Loans (Under $120,000 AGI)

This will generally impact new graduates fresh out of optometry school since their starting salaries are drastically lower. If you have not done so, remember to apply for $10,000 one-time student loan debt relief via federal application here. Please note that due to a court order, debt discharge is paused until further notice.

Our advice is if you are NOT planning to go for loan forgiveness, leave $10,000 aside as federal loans, and consider refinancing the rest of your student loans before 11/30/22 to take advantage of the lowest rate.

If you are still hesitant, it is definitely okay to wait as we get closer to 12/31/22 but you risk refi rates climbing up.

Please have a solid financial game plan when it comes to your student loans. Don’t get caught by surprise when repayment resumes and you are stuck with a 6.8% federal rate and unable to refinance to a lower rate. Try to have a goal to pay off your student within 5-10 years!

Scenario #2: Optometrists with Federal Student Loans (Over $120,000 AGI)

Our advice is still the same for all ODs with federal loans, if you are not planning to go for loan forgiveness, consider refinancing your student loans before 11/30/22 to take advantage of the lowest rate, essentially saving 1.00% compared to refinancing in 2023.

One month of federal 0% interest saving is NOT worth getting a higher rate especially if you are signing up for a longer term like 10 or 15 years.

Continue to aggressively pay off your student loans with the goal to be done within 5-10 years.

Scenario #3: Optometrists Who Refinanced Their Student Loans

You are probably one of the lucky ODs who got that super low interest rate of 2-3% back in 2020, so continue your financial plan and keep aggressively paying off that student debt each month with the goal of finishing off within 10 years. Any extra cash flow goes into debt payment or investment.

Scenario #4: Optometrists within 10 years Public Service Loan Forgiveness (PSLF)

The last 2+ years have been awesome for all the PSLF ODs out there, you had zero monthly payments but had over 24+ qualified payments count toward your 120 total payments.

So continue enjoying the 0% interest and DO NOT make any payments until 1/2023. Start planning to resume your federal loan payment and watch out for any update to the new income-based repayment plan starting in 2023.

Financial Pearl

"If you have any federal payments that you are unsure will count toward PSLF but missed the limited PSLF waiver submission (expired 10/30/22), don’t worry, there will be a one-time income-driven relief (IDR) account adjustment (around July 2023). This will continue to count payments toward PSLF (with qualifying employment) by consolidating payment by 5/1/2023 if you have ineligible loans. This is expected to be a permanent improvement to the PSLF forgiveness program.

For all optometrists in any forgiveness programs, we highly recommend consulting with Patrick Logue CFP for a full student loan plan (25% discount for ODoF members: $296)

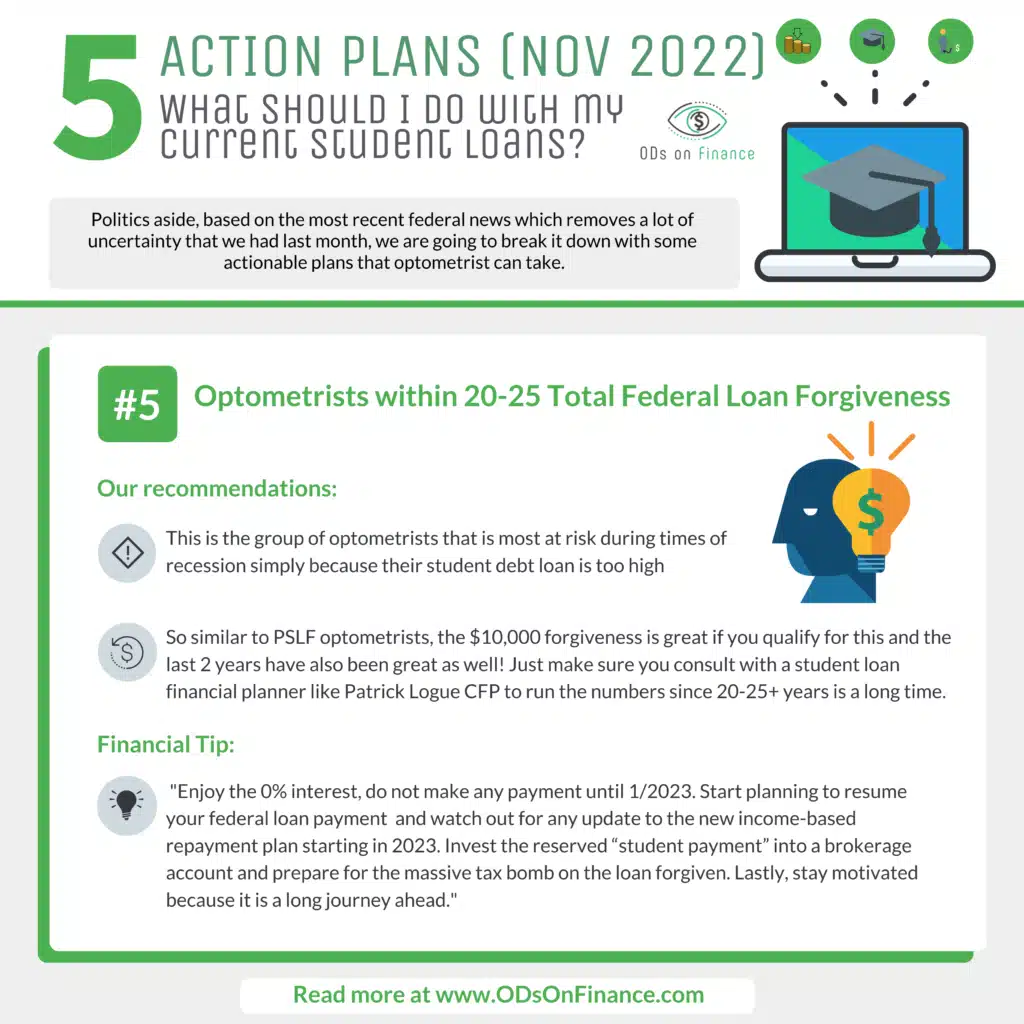

Scenario #5: Optometrists within 20-25 Total Federal Loan Forgiveness

This is the group of optometrists that is most at risk during times of recession simply because their student debt loan is too high. While we are advocates for debt payment, we acknowledge that mathematically speaking, optometrists with a massive debt load (ex: $300,000 debt, while still making $100,000 annually, so a greater than 3:1 DTI Ratio) will have a difficult time paying off debt, while investing for retirement unless their salary drastically increases…or they literally LIVE ON BEANS/RICE for many years.

So similar to PSLF optometrists, the $10,000 forgiveness is great if you qualify for this and the last 2 years have also been great as well!

Enjoy the 0% interest, do not make any payment until 1/2023. Start planning to resume your federal loan payment and watch out for any update to the new income-based repayment plan starting in 2023. Invest the reserved “student payment” into a brokerage account and prepare for the massive tax bomb on the loan forgiven. Lastly, stay motivated because it is a long journey ahead."

Again, definitely do a consult with a student loan financial planner like Patrick Logue CFP to run the numbers since 20-25+ years is a long time to make sure everything is properly allocated.

Financial Calculator

"Got massive optometry student loans and stressed out by all the federal payment payment?

Check out our FREE & comprehensive OD-Focused repayment calculator that can compare all the federal income-based repayment such as PAYE, REPAYE and refinancing options, to see if federal forgiveness is the right path for you! Or saving thousands by refinancing to a lower interest. Click here to run your own student loan analysis"

Summary:

As we are preparing to head into a deeper recession in 2023 with unprecedented high inflation and higher unemployment rates, it is vital for optometrists to have a solid financial plan when it comes to your student loans.

Our advice is always the same; have a comprehensive financial plan and stick to it, have a solid 6-months emergency fund, don’t take on too much debt, cut down your budget/expenses, & continue investing in a broad-market, low cost, index fund each month!

Remember that even in a recession, we are fortunate as doctors that people still need eye exams, so practice owners, continue working to build your practice and work to cut down on cost and improve efficiency. Associate ODs, continue working hard and being that rockstar OD! Now is definitely not the time to quiet-quit especially in a recession.

As always, we are all in this together with 15,500+ optometrists staying strong, so stay motivated!

-Dat & Aaron | Co-Founders

")

Want to learn how to refinance your student loans? Check out The Optometrist's Guide to Student Refi

Want to check out the Lowest rate + Best Deals? Compare Recommended Student Loan Refi Lenders

Facebook Comments